The acquisition of Discover by Capital One will certainly strengthen the Discover network relative to MasterCard and Visa. However, the acquisition will likely not move the needle in any material way as payments industry volume remains heavily concentrated among the largest U.S. banks who compete directly with Capital One. The risk to MasterCard and Visa will come from how large banks respond to a competitive market advantage Capital One gains by acquiring Discover.

Large Bank Volume Will Eventually Migrate Off MasterCard and Visa

Capital One will over time migrate its MasterCard and Visa card volume to the Discover network. At full migration and current card purchase volumes, MasterCard and Visa combined would lose over $1.3 billion a year in revenue related to Capital One’s card business. Notwithstanding the financial impact, that in of itself is not going to dramatically change MasterCard and Visa in the U.S.

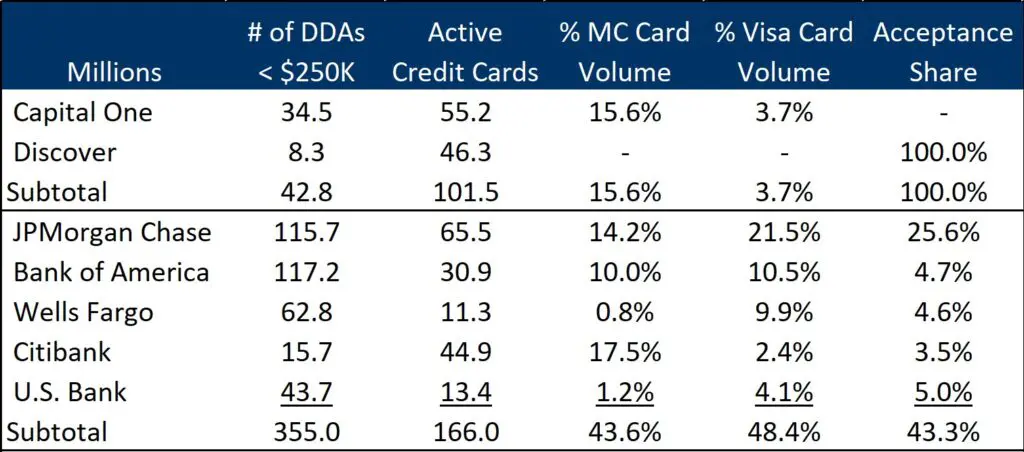

2024 Key Statistics[1]

How the very largest U.S. banks (with nearly half of U.S. payments volume) respond to what Capital One can do with the Discover network could dramatically change MasterCard’s and Visa’s role in the industry.

Private / Closed Networks Will be Required to Compete with Capital One

Chase partnered with Visa years ago to allow it to offer customized merchant pricing (discount rates/interchange) when a transaction at a Chase acquired merchant is conducted by a Chase Visa cardholder (ChaseNet). The volume through ChaseNet is not publicly available, but Chase’s overall lack of meaningful acquiring share gain since launch suggests its private/closed network has been used more defensively to protect existing merchant acquiring and credit card issuing co-brand relationships. Chase still requires Visa to provide national and international network coverage for cardholder purchases at non-Chase merchant locations.

The challenge for Chase and any other large banks that may have network aspirations to achieve the benefits of vertical integration is that Capital One has strategically leap frogged them and has access to every merchant in the U.S. that accepts Discover. When combined with Capital One Discover’s card scale and its ability to, among others, minimize regulatory impact (closed networks are not subject to Durbin on debit or the proposed credit card competition act), Capital One can now create any number of competitive value propositions that mutually benefit merchants, cardholders, and Capital One.

Capital One will have a financial advantage relative to other card issuers as it gains acquiring revenue or value (that otherwise would have gone to MasterCard or Visa) on each transaction that could be used to increase cardholder rewards. This advantage grows as they combine with the debit rewards offered by Discover today. In addition, Capital One can lower merchant fees, develop enhanced rewards and/or cardholder experiences, establish more compelling co-brand programs, and/or pull any number of levers to achieve Capital One’s stated goal of using Discover to enhance its “ability to compete with the nation’s largest banks in credit cards and banking”.[2] The end game for Capital One is to not just monetize the 38 million or more Discover cardholders that do not bank with Discover Bank today or to grow its cardholder base, but to ensure that it will be one of a finite number of industry “survivors”.

Certainly, the largest banks can compete over the short-term by reducing costs or even taking lower margins on payments industry services. Longer-term, Chase, Bank of America, and others will have to respond accordingly to protect and grow their respective payments businesses. And in most scenarios, it will lead to a material reduction in MasterCard and Visa payment network volume and revenue.

American Express Has To Be In Play

Strategically, acquiring American Express may be the only path for the largest banks to replicate and maybe even enhance on Capital One Discover. Only Chase, Bank of America, and possibly Wells Fargo could effectively pull this acquisition off based on market capitalization; although Chase would likely have greater regulatory concern as both American Express and Chase have similar annual purchase volumes.

Key Industry Participants[3]

Acquiring American Express would allow any of these large banks to establish their own private network that would be at relative parity with Capital One Discover, migrate sizeable volume off MasterCard and/or Visa, and ensure their long-term industry “survival.”

Could Fiserv/First Data Play a Role?

MasterCard and Visa are incredibly valuable assets – although probably half of their market capitalization is from international business. We believe legacy First Data has it ingrained in their DNA to someday displace Visa in the U.S. and take advantage of the valuable economics associated with payment networks. Fiserv has amassed sizeable endpoints (core bank processing, merchant acquiring) that they could leverage to create a credit card network alternative to MasterCard and Visa; particularly with community financial institutions. However, replicating what MasterCard and Visa have built and gaining national acceptance will be challenging for a variety reasons, including not having a meaningful consumer brand.

The more immediate play could be to facilitate one or more merchant partner or processed banks (Bank of America, Wells Fargo, PNC, and/or Citibank) in creating a sizeable Fiserv/bank network that could create closed or on-us value for participating card issuers. We expect there to be a relatively high density of volume (most acquired volume is likely within the bank’s combined footprint) that could make this work, but large bank control or influence would make execution challenging. And all issuers will still need MasterCard or Visa for national and international coverage over the near-term.

What Will Likely Happen?

We expect that American Express will eventually be acquired and, if it is by Chase, as much as 30% of MasterCard’s and 25% of Visa’s payments volume will migrate to Chase and Capital One’s closed networks. And as the likely chaos unfolds for the remaining banks, we expect to see a rationalization of banking and merchant acquiring assets. It is hard to believe that Worldpay/Global with a combined 25% or so share of the acquiring market would not be acquired by one of the remaining large banks. Gaining control/influence over these merchant endpoints will be much more effective than trying to sell bank-owned network acceptance to these or other merchants.

The remaining largest banks will look to MasterCard and Visa to level the playing field and we believe both will eventually offer an expanded ChaseNet relationship to a finite number of card issuers. MasterCard and Visa will either private label their national network or allow the card issuer more control or influence over the network fees, interchange, rules, and other aspects associated with the issuers card volume such that the card issuer can compete more effectively against Capital One Discover and whatever bank acquires American Express. It is in MasterCard’s and Visa’s best interest to participate in and manage the decline in this card volume as the banking and acquiring industry consolidates.

And while MasterCard or Visa will certainly push back initially, we fully expect this relationship to get implemented as any challenger brand will be much more accommodating to the issuer’s requirements. Any lost revenue will adversely impact the incumbent’s market capitalization and shareholders.

At the end of the day, MasterCard and Visa will remain longer-term industry players as half of the market (outside the largest banks) will most likely be conducted over their respective networks. However, the balance of power in acceptance negotiations and the scope of network services provided to card issuers, among others, will have to change over time as MasterCard’s and Visa’s business in the U.S. become smaller. Issuers will need to consider a world where network fees go up, interchange goes down, and the amount of value issuers receive from networks (e.g., marketing, promotion, sponsorship, consulting/advisory, product support, etc.) go away or are severely limited.

Scott Reaser (Partner), with over 25 years of industry experience, manages McGovern Smith Advisors Strategic Sourcing practice. He can be reached at [email protected]

[1] Nilson Report, financial condition reports, and McGovern Smith estimates and analysis. Card volume includes dual-message credit and debit. Acceptance Share for banks represent % of acquired MasterCard and Visa volume.

[2] Capital One February 2024 investor presentation.

[3] Reflects 2018 pre-merger market cap of Fiserv and First Data. Source: companiesmarketcap.com