McGovern Smith’s analysis of covered U.S. issuers (i.e., those financial institutions with over $100 billion in assets under the proposed act) and the network fees tied to their credit card volume suggests a pending storm for exempt and some covered financial institutions. While credit interchange declines get the headline (and deservedly so after debit and the Durbin Amendment), an under the radar aspect of the pending legislation is the potentially dramatic rise in MasterCard/Visa network fees facing exempt credit card issuers and others.

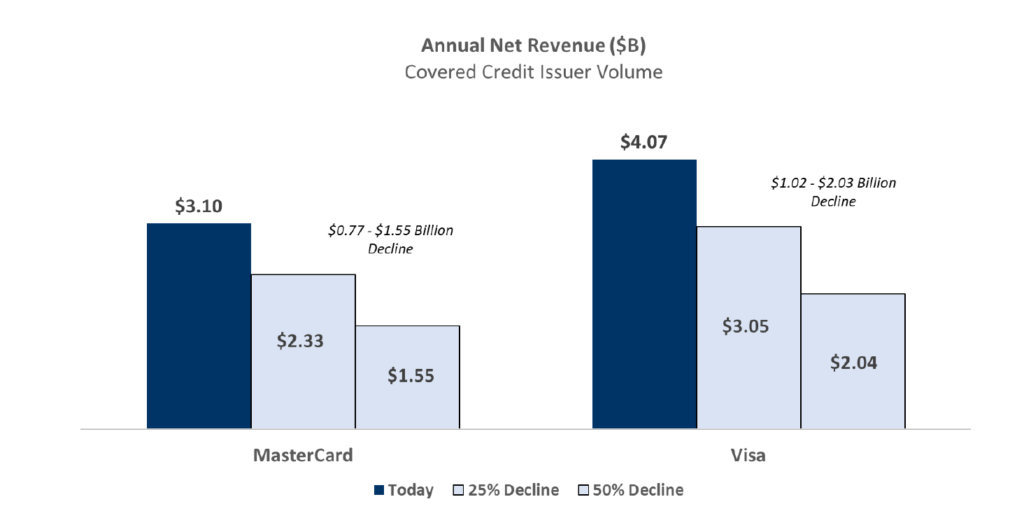

McGovern Smith estimates MasterCard and Visa earn $3.1 billion and $4.1 billion a year, respectively, in network fees tied to covered issuer credit card network volume. This revenue will be at considerable risk of decline should one or more challenger networks (i.e., American Express, Discover, Fiserv/Star, or other network.) gain traction – generally requiring fee increases by MasterCard and/or Visa to largely maintain network economics without diminishing services, operations, and issuer support levels. And since the largest banks and merchants will largely remain unaffected fee wise, exempt financial institutions, smaller covered issuers, and small to mid-size merchants will bear the brunt of any network volume decline. A 25% to 50% reduction in covered issuer credit card volume could cause a ~$1 to $2 billion a year revenue shortfall at MasterCard and Visa.

MasterCard and Visa will certainly rationalize some operations and delivery should the proposed legislation go into effect. However, their respective value propositions are tied to the product, innovation, technology, staff, marketing, program and other support offered to network participants. This is not easily replicated by other networks and will be a key source of differentiation competing for the largest issuers in the U.S. This suggests that existing delivery and capabilities will largely be retained and that one or both networks will look to fee increases to offset any revenue shortfall.

To the extent MasterCard or Visa target exempt and smaller covered credit card issuers to recover the majority of any revenue shortfall, these institutions could see network fees double or even triple the rates currently paid for credit card network services. Material network fee increases to exempt credit card issuers along with any decline in interchange would make it very challenging for community banks and credit unions to compete effectively and profitably in the credit card market.

Not all issuer fee increases would be obvious; although increases in cross-border, core, or quarterly service fees would. The biggest contributor to fee increases is expected to be in the loss of or reduction in financial incentives or other benefits (such as product support or consulting/advisory) in existing and go forward network agreements. Financial incentives have historically been the primary mechanism used by networks to discount issuer fees. Should these go away or be greatly diminished, exempt issuers and smaller covered issuers could incur material credit card network fee increases.

Issuers of all sizes should review their participation agreements and determine the implications of one or more of the following should the proposed or similar legislation go into effect:

- Program requirements or volume triggers that eliminate incentives or benefits altogether or cause possible termination and/or renegotiation of network agreements.

- Volume-based or growth-based incentives or benefits that decline as volume shifts to other competing networks.

- Fee elements that are not subject to fee escalator protection or the lack of fee element escalator protection altogether.

Will the dramatic increase in network fees occur over night? Highly unlikely as network alternatives would need to effectively cover the full spectrum of card programs that MasterCard and Visa credit card issuers offer today. However, over the near term we expect restructuring of issuer relationships that are set to expire to alter financial incentive structures and triggers, reduce program and/or account management support, and provide payments networks the ability to more readily raise fees.

Scott Reaser (Partner), with over 25 years of industry experience, manages the Strategic Sourcing practice at McGovern Smith Advisors. He can be reached at sreaser@mcgovernsmithadvisors.com