The payments industry has seen dramatic changes over the past few years with industry consolidation and the Covid-19 pandemic. However, after the dust has settled, card processor operating costs (on a per transaction basis) continue to decline highlighting the inherent scale in card issuer processing businesses. And so long as credit and debit card processing pricing remain largely variable in nature, driven by underlying transaction growth, the decline in processor operating costs should be followed closely and factored by card issuers into their renewal and sourcing processes.

McGovern Smith developed a Processor Cost Index derived from SEC filings, industry statistics, and other public information that measured the decline in third party card processing unit costs. The latest version has been expanded to reflect a greater share of industry transactions – partially driven by industry consolidation and partially to mitigate the impact of other services beyond card processing and related services (e.g., ATM driving, EFT network, back-office, etc.) in reported segment financials.

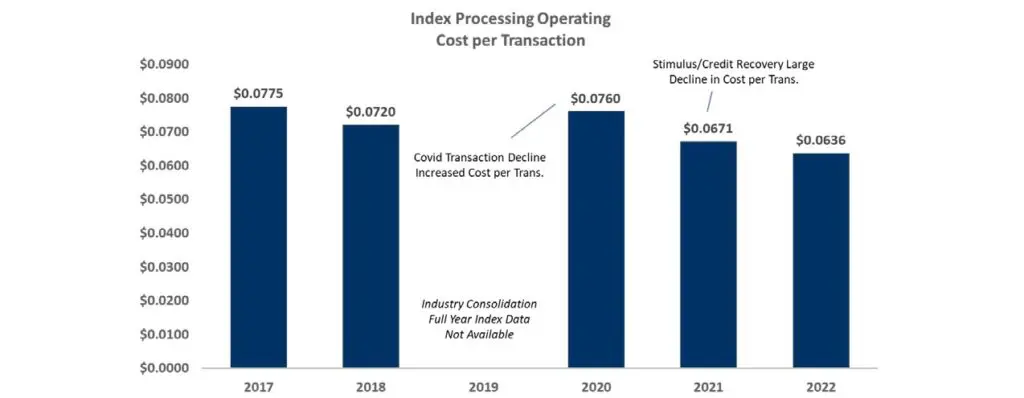

The chart above shows that aggregate processor operating cost per transaction continues to decline over time. While we would expect 2019 to be lower than 2018 (full year data was not available), the 2020 increase over 2018 levels was an anomaly as industry transactions declined due to Covidlockdowns and business shutdowns/restrictions. Unless another disruptive event hits the industry or more modern platforms win considerable market share from legacy players, processors will continue to disproportionately benefit from platform scale and declining operating unit costs.

Issuer card processing contracts executed in 2017 and early 2018 should target unit cost savings of 18% today to mirror the decline in processor operating costs per transaction over the past 5 years. While analysis of this type is susceptible to accounting and reporting practices of processors, it is important to note that 18% savings is consistent with the floor savings results achieved by McGovern Smith during recent client engagements; although several other client engagements have approached savings of 29% compared to current or baseline pricing.

While the index results should be targeted by many institutions for their respective businesses, individual savings results will be influenced by a variety of factors, including (among others):

- Services mix – back-office services generally contribute very little to available fee savings compared to scalable core processing and related services;

- Process employed – renewal negotiation versus competitive or RFP process;

- Nature of the relationship – stand-alone versus enterprise vendor relationship;

- Delivered volume, scope of processing services, and any new services contemplated;

- Hidden costs (e.g., API/data access fees in a digital environment) and contractual provisions that re-capture costs (e.g., CPI fee escalators); and,

- Results achieved during the institution’s last processor negotiation.

Certainly, the current inflationary economic environment, past and future platform investment (e.g., cloud, digital, etc.) and other tactics will influence how a processor positions available savings in today’s market; however credit and debit card issuers will still need to take advantage of scale benefits that processors have achieved over time.

Scott Reaser (Partner), with over 25 years of industry experience, manages the Strategic Sourcing practice at McGovern Smith Advisors. He can be reached at sreaser@mcgovernsmithadvisors.com

McGovern Smith Advisors – Payments Strategic Sourcing Offerings