In April, FIS announced its acquisition of the Issuer Solutions Business of Global Payments in conjunction with the sale of the Worldpay merchant acquiring business to Global Payments. As currently structured, the FIS acquisition of TSYS requires the simultaneous closing of Global Payments / Worldpay with both deals predicated on relatively standard closing conditions being met and regulatory approval of the other.

And while the deal is somewhat complex (tying card processing and merchant acquiring deals together), nothing in the transaction agreement suggests the deals are unlikely to close (absent regulatory approval). The greatest risk to FIS TSYS closing is obtaining regulatory approval for both transactions.

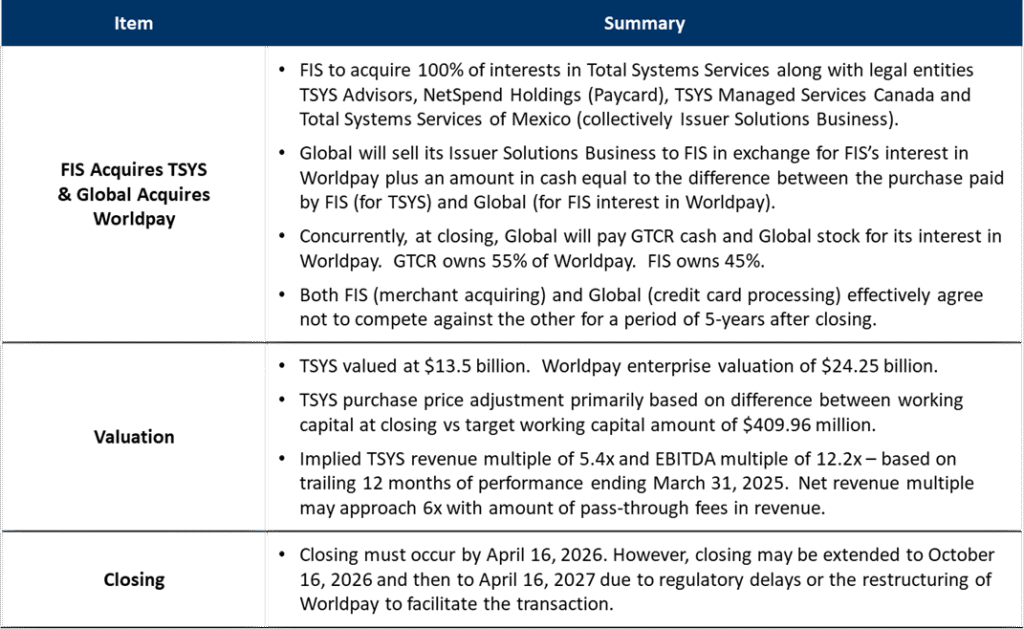

FIS is Acquiring 100% of the Stock of TSYS

The issuer processing business of TSYS is a Delaware LLC (Total Systems Services) and is separate and distinct from any acquiring assets of Global (including the legacy acquiring assets of TSYS). FIS is acquiring the issuer processing business of TSYS along with related legal entities TSYS Advisors, TSYS Managed Services Canada and others.

A summary of key aspects of the transaction agreement is provided below.

U.S. Regulatory Approval May be Dependent on How a Market is Defined

The Department of Justice and Federal Trade Commission use the Herfindahl-Hirschman Index (“HHI”) to determine market concentration when approving mergers and acquisitions. According to the DOJ, “HHI is calculated by squaring the market share of each firm competing in the market and then summing the resulting numbers. For example, for a market consisting of four firms with shares of 30, 30, 20, and 20 percent, the HHI is 2,600. The agencies generally consider markets in which the HHI is between 1,000 and 1,800 points to be moderately concentrated, and consider markets in which the HHI is in excess of 1,800[1] points to be highly concentrated. Transactions that increase the HHI by more than 100 points in highly concentrated markets are presumed likely to enhance market power.”

Defining a market or a market’s structure is complex. It is very much situational and the DOJ and FTC have discretion to apply its merger guidelines/framework “reasonably and flexibly to the specific facts and circumstances of each merger.” The following analysis should be viewed with caution as our view of the market could differ considerably from the DOJ or FTC and is based on available (and potentially inaccurate) industry data and assumptions. This analysis is intended to frame the potential outcome using HHI estimates. It is important to note that the agencies will frame the market as they choose but will also do so with much greater information.

In terms of market structure, we excluded in-house bank issuer processors (e.g., JP Morgan Chase) although we do highlight the impact for credit card processing given it is a highly concentrated market. The merger guidelines allow the inclusion of in-house providers if they could offer their services third party and/or have influence over the supply chain. While Chase and other banks could sell processing third party, the reality is that large banks and others will not process with a bank competitor that has access to their cardholder data, pricing, and other program information. As such, we excluded in-house bank processors but the agencies could certainly include in their analysis.

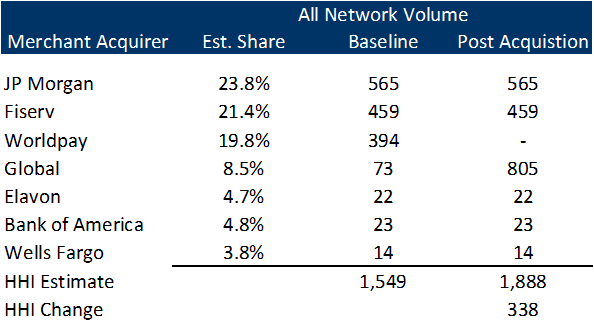

Merchant Acquiring Market Structure Could be Problematic

We defined the market for merchant acquiring to be ownership (including partial ownership) of merchant contracts with HHI measured based on total purchase volume (MasterCard, Visa, American Express, PIN-debit) as reported in the Nilson Report and our industry share estimates.

Merchant Acquiring HHI Estimates

[1] In December 2023 Merger Guidelines (DOJ / FTC), the threshold was lowered from 2,500 to 1,800.

Based on current guidelines, the market is moderately concentrated prior to the Worldpay acquisition, but exceeds the highly concentrated market threshold post Global acquisition. To the extent the agencies use processing (rather than ownership) as the market (which is more difficult to frame as entities or ISOs may have multiple front-ends), we would expect the pre-acquisition HHI to exceed 1,800 and post-acquisition to increase well over 100 points.

We expect the agencies to spend appropriate time evaluating the market structure and impact of the Worldpay acquisition by Global. Should the merchant acquiring deal not gain approval by the DOJ and/or FTC, the FIS acquisition of TSYS is unlikely to move forward.

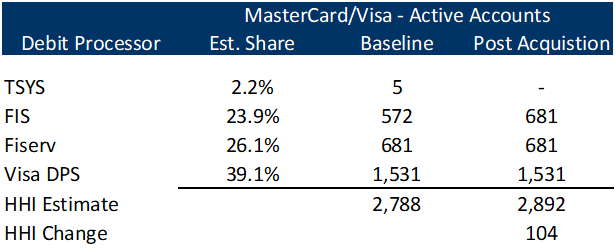

Debit Card Processing is Already Highly Concentrated

We defined the market for debit card processing to be MasterCard and Visa active debit card accounts based on Nilson Report data, company public filings, and our industry share estimates. Prepaid was excluded due to a large number of accounts but small annual transaction volume – this highlights the challenges to agencies in term of how to frame the market and which evaluation metric to use. Should prepaid be included, we would expect agencies to use transactions as the relevant metric. However, the HHI result would likely be much worse than below as the largest banks tend to have greater transactions per active and disproportionately process using Visa DPS.

Debit Card Processing HHI Estimates

Likewise, the agencies could perform the analysis including banks that issue Discover debit cards; although the volume is not available publicly and the likely small number of active accounts would likely have a negligible impact on the results.

While the market is highly concentrated pre-acquisition, the relatively low TSYS market share yields an HHI increase of slightly over 100 post-acquisition. Notwithstanding the HHI, there is a reasonable argument that FIS acquiring TSYS would not increase market power in any meaningful way. TSYS has never been a major debit player and its growth has been constrained by not having a PIN-debit network or ATM processing capabilities (services generally sold in conjunction with debit processing services). We believe the agencies will likely approve the debit component of the transaction.

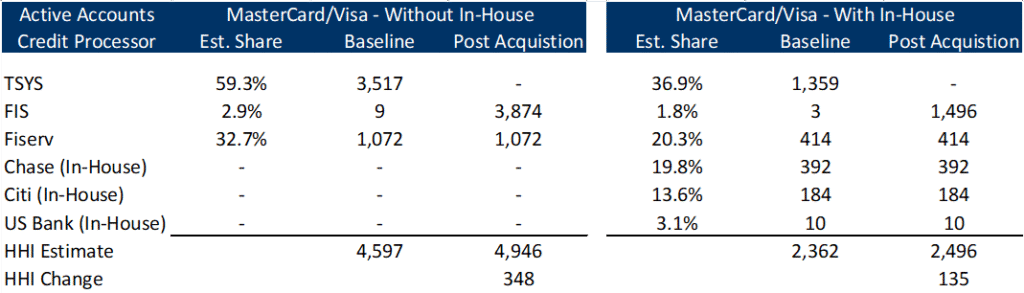

Will FIS have to Divest its Existing Credit Card Processing Business?

We defined the market for credit card processing to be MasterCard and Visa active credit card accounts (consumer, small business, retail, and commercial card)[2] based on Nilson Report data, company public filings, and our industry share estimates. It is quite possible the agencies look at credit and debit processing as a combined market rather than individual markets or even include Discover or American Express in its credit card market structure. We believe the credit and debit processing markets are sufficiently different in terms of how the products are sold to and purchased by issuers (very infrequently are they purchased together) and the barriers to entry are significantly greater with credit card processing.

The credit card processing market is highly concentrated with two leading third-party processors – TSYS and Fiserv. The HHI remains high even after factoring in active accounts associated with in-house credit card processors. And while the credit processing share of FIS is relatively small, we expect the agencies to focus on the competitive implications of having only two major third party processors remaining in the industry.

[2] Store cards are excluded but would likely yield an even more concentrated market.

Credit Card Processing HHI Estimates

While it is possible the agencies will approve the credit card component based on how they define the market, we believe it is more likely that either FIS will offer to or the agencies will require FIS to divest its credit card processing business to move forward with the TSYS acquisition. FIS built a relatively new credit card processing platform (Payments One Credit) with the objective of targeting larger U.S. financial institutions and credit card issuers. This platform is separate from debit and could be competitively used by any number of players, new entrants, or others to grow business and third-party market share and increase credit card processing competition.

At the end of the day, the FIS acquisition of TSYS will be driven by the analysis performed by agencies on the card issuing processing and merchant acquiring markets. We have highlighted potential challenges based on our HHI estimates but expect the card processing component of the transaction to ultimately gain approval (with the potential for FIS to divest its Payments One Credit processing business). How the agencies view the Worldpay acquisition by Global Payments is more unpredictable but there would still be a healthy number of key players and competition remaining in the market place. To the extent the merchant acquiring component gains regulatory approval, there appears to be a strong likelihood FIS TSYS will close at some point in 2026.

Scott Reaser (Partner), with over 25 years of industry experience, manages McGovern Smith Advisors Strategic Sourcing practice. He can be reached at sreaser@mcgovernsmithadvisors.com